Key Takeaways:

- AI detects and prevents fraud in real time and reducing financial loss.

- Machine learning adapts to new fraud tactics, unlike traditional rule-based systems.

- Businesses across banking, e-commerce and healthcare use AI to improve fraud prevention.

- Strong data compliance and continuous monitoring are essential for successful AI fraud detection.

What if a fraudster could steal money from your business in seconds without being detected?

As digital payments, online transactions, and cloud services continue to grow, businesses face increasing risks from payment fraud, identity theft, cyberattacks, and deepfake scams. Traditional fraud detection methods often struggle to keep up with these evolving threats.

This is where AI in fraud detection makes a difference. By analyzing large volumes of data in real time, AI can identify suspicious activities, reduce fraud risks, and improve security.

In this blog, we’ll cover how AI fraud detection works, its key benefits, implementation process, industry use cases, and compliance considerations.

What is AI Fraud Detection and Prevention?

AI fraud detection is the use of artificial intelligence and machine learning to identify, prevent, and respond to fraudulent activities in real time.

Generally, instead of relying on fixed rules like: “If a transaction is above $10,000, block it,”

AI systems study large amounts of past data to understand what normal behavior looks like. Then, they detect unusual or suspicious actions that may indicate fraud. This makes artificial intelligence in fraud detection much more flexible and accurate than traditional rule-based systems.

Rule-Based vs. AI-Based Fraud Detection

| Factor | Rule-Based Systems | AI-Based Systems |

| Adaptability | Fixed rules, updated manually | Learns continuously from new data |

| Detecting unknown fraud | Misses patterns outside the rules | Detects new and emerging fraud tactics |

| False positives | Tend to be higher | Lower, due to deeper behavioral context |

| Speed | Fast, simple checks | Fast, but needs real-time infrastructure |

| Explainability | Easy — “Rule X triggered” | Needs added tools (e.g., SHAP) for transparency |

| Best fit | Simple, well-known fraud types | Complex, evolving, and networked fraud |

Most businesses use rules and AI together, rules catch known fraud, while AI detects new and complex threats.

How Artificial Intelligence in Fraud Detection Works

Artificial intelligence in fraud detection works by collecting and analyzing many types of data to understand user behavior and detect suspicious activity. AI systems examine transaction data such as the amount, time, and location of a payment. They also study user behavior data, like how a person normally logs in, shops, or transfers money.

In addition, the system gathers device information, including IP address, device type, and browser details. It may also use biometric data such as face recognition or fingerprint scans, along with geolocation signals that show the physical location of the transaction.

After collecting this information, AI models compare each new activity with the user’s past behavior. If something looks unusual, the system assigns a risk score to the action.

Based on this score, the AI system can automatically approve the transaction, block it, or flag it for manual review. This complete process is called fraud detection using AI, and it happens within seconds to prevent financial loss and protect users.

Supervised vs. Unsupervised Learning

AI uses two main learning methods to detect fraud:

- Supervised Learning

- Trains on historical data that is already labeled as “fraud” or “not fraud.”

- Works well for detecting known and common fraud patterns.

- Unsupervised Learning

- Does not require labeled data.

- Identifies unusual patterns or outliers in data.

- Helps detect new and emerging fraud tactics.

By combining both methods, AI-powered fraud detection systems become smarter, faster, and more effective than traditional fraud detection systems.

Core AI Models Used in Fraud Detection

Real fraud detection systems rarely rely on just one algorithm. Most teams combine several models, each suited to a different type of fraud signal.

- Random Forest: Builds many decision trees and combines their results. It handles missing data well and resists noisy labels, which makes it a solid baseline model for transaction scoring.

- XGBoost (Extreme Gradient Boosting): Builds trees one after another, with each new tree correcting the errors of the last. It is the most widely used algorithm for scoring individual transactions because it trains fast and handles large tabular datasets with high accuracy.

- Isolation Forest: An unsupervised model that isolates outliers instead of learning from labeled fraud cases. Because it doesn’t need historical fraud data, it’s useful for catching new fraud patterns that haven’t been seen before.

- Autoencoders and Neural Networks: These models learn what “normal” behavior looks like and flag activity that deviates from it. They work well for behavioral biometrics, such as typing speed or mouse movement, where patterns are too complex for simple rules.

- Graph Neural Networks (GNNs): Fraud is rarely committed by a single account acting alone. GNNs map the relationships between accounts, devices, IP addresses, and merchants to uncover fraud rings, mule accounts, and synthetic identity networks-connections that transaction-level models miss because they evaluate each transaction in isolation.

Which AI Model Fits Which Fraud Problem

| Model | Best Suited For | Data Needed | Limitation |

| Random Forest | General-purpose transaction scoring | Labeled fraud / non-fraud data | Slightly less accurate than boosting on clean data |

| XGBoost | High-volume, single-transaction fraud (card payments) | Large labeled dataset | Needs regular retraining as fraud patterns shift |

| Isolation Forest | New or unknown fraud patterns | No labels required | Higher false-positive rate than supervised models |

| Autoencoders / Neural Networks | Behavioral biometrics, complex non-linear patterns | Large volume of behavioral data | Harder to explain to regulators (the “black box” problem) |

| Graph Neural Networks (GNNs) | Fraud rings, mule accounts, synthetic identities | Relationship data (device, IP, account links) | Computationally heavier; needs graph infrastructure |

AI in Fraud Management Market Size

The global AI in Fraud Management Market is expected to grow significantly over the next decade, reaching USD 95.11 billion by 2036 at a CAGR of 18.5%. This growth is driven by increasing demand for real-time fraud detection, identity verification, and automated risk management solutions.

AI-powered fraud prevention software is projected to hold 57.3% of the market, reflecting the shift toward intelligent and proactive fraud prevention systems. Additionally, countries such as China and India are emerging as some of the fastest-growing markets due to rapid digital adoption and expanding online transactions.

Importance of Fraud Detection in the Digital Landscape

As digital payments, online shopping, and mobile banking grow, fraudsters are also becoming smarter. Businesses lose millions of dollars every year due to cyber fraud, identity theft, and fake transactions. This is why strong fraud detection systems are essential for survival and growth in the digital age.

Let’s understand why fraud detection is so important today.

1. Prevent Financial Loss

Fraud can cause serious financial damage to businesses and customers. Stolen credit cards, fake insurance claims, and hacked bank accounts can result in huge losses within minutes. AI for financial fraud detection helps detect suspicious transactions instantly and blocks them before money is lost.

2. Protect Customer Trust

Customers share sensitive information like card details, addresses, and ID proofs with companies. If fraud happens, customers may lose trust and stop using the service. AI in fraud prevention protects user data and ensures safe transactions, which helps businesses maintain strong and long-term customer relationships.

3. Maintain Brand Reputation

A single fraud incident can damage a company’s public image. News about data breaches spreads quickly and can harm the brand’s credibility. AI fraud detection software reduces the chances of such incidents and protects the company’s reputation in the market.

4. Meet Legal and Regulatory Rules

Financial institutions must follow strict laws and compliance standards to prevent fraud and money laundering. Failure to comply can lead to heavy fines and legal trouble. Artificial intelligence for fraud detection helps companies monitor transactions properly and meet regulatory requirements efficiently.

5. Improve Operational Efficiency

Traditional fraud detection depends heavily on manual reviews, which take time and effort. Employees may spend hours checking suspicious cases. AI automates this process, reduces manual workload, and allows teams to focus on more important and complex tasks.

6. Reduce False Positives

Older systems often block genuine customers by mistake, which creates frustration and a poor user experience. AI systems are more accurate because they analyze behavior patterns deeply. This reduces unnecessary transaction blocks and improves customer satisfaction.

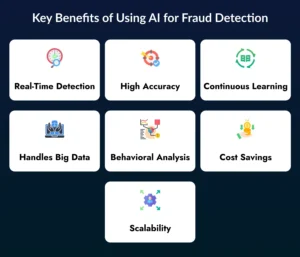

Key Benefits of Using AI for Fraud Detection

Using AI in fraud detection provides several powerful advantages that help businesses stay secure and efficient.

- Real-Time Detection: Analyzes transactions instantly and identifies suspicious activity before significant damage occurs.

- High Accuracy: Detects hidden fraud patterns while reducing false positives and false negatives.

- Continuous Learning: Adapts to new fraud tactics by learning from fresh data and fraud cases.

- Big Data Processing: Handles and analyzes millions of transactions efficiently without impacting performance.

- Behavioral Analysis: Monitors user behavior patterns to identify unusual or suspicious activities.

- Cost Savings: Reduces fraud losses, lowers investigation costs, and improves operational efficiency.

- Scalability: Easily supports growing transaction volumes while maintaining speed and accuracy.

Key Challenges in AI Fraud Detection

Implementing AI in fraud detection is complex. Businesses must plan carefully to make the system work properly. Below are the main challenges and their solutions.

1. Data Quality and Availability

Artificial intelligence in fraud detection depends on data. If the data is incomplete, incorrect, or too small, the model will not work properly. Small companies may struggle to collect enough labeled fraud data.

To succeed, businesses must build a strong data collection system before deploying AI fraud detection.

2. Managing False Positives

Even the best AI fraud detection software can sometimes flag genuine users as fraudsters. This creates frustration and poor customer experience.

Companies must regularly monitor model performance, adjust risk scores, and keep human experts involved to review sensitive cases.

3. Model Explainability (The “Black Box” Problem)

Some AI models, especially deep learning systems, do not clearly explain why they blocked a transaction. This can create problems for regulators and customers.

Using simpler models where possible and keeping humans in the loop improves trust in artificial intelligence for fraud detection.

4. Real-Time Infrastructure Demands

Fraud detection using AI must work in milliseconds. This requires strong servers, fast databases, and real-time processing systems.

Without proper infrastructure, AI integration in fraud detection may become slow and ineffective.

Step-by-Step AI Fraud Detection Implementation Process

Deploying AI fraud detection isn’t a single project, it’s a sequence of decisions that determine whether the system actually reduces fraud without blocking genuine customers.

Here is the implementation process:

1. Define Objectives

Before writing a line of code, decide which fraud types matter most (card fraud, account takeover, fraud rings), what false-positive rate the business can tolerate, and what budget and timeline are realistic. This shapes every decision that follows.

2. Collect and Integrate Data

Pull together transaction logs, device and browser fingerprints, behavioral data, and historical fraud labels from existing systems such as the payment gateway, core banking platform, or CRM. Most AI fraud projects stall here, not at the modeling stage, because the data lives in disconnected systems.

3. Clean Data and Train Models

Prepare the data by removing duplicates, filling in missing values, and creating useful fraud indicators, such as transaction frequency and unusual spending behavior. The cleaned data is then used to train AI models for accurate fraud detection.

4. Validate and Add Explainability

Backtest the model against historical, confirmed fraud cases before it ever touches live transactions. For any model going into production, add an explainability layer (such as SHAP or LIME) so analysts and regulators can see why a transaction was flagged.

5. Integrate With Existing Systems

Connect the model to the payment gateway or banking core through APIs so it can score transactions in real time. This stage typically requires the most engineering effort, since the system must return a decision in milliseconds without slowing down checkout or login.

6. Set Decision Thresholds and Workflows

Define what happens at each risk score: auto-approve, auto-block, or route to a human reviewer. Getting these thresholds wrong in either direction either lets fraud through or frustrates genuine customers.

7. Deploy in Shadow Mode, Then Go Live

Run the new model alongside the existing system without letting it make real decisions yet. Compare its flags against what actually happened, fix issues, and only then let it start blocking or approving transactions on its own.

8. Monitor and Retrain Continuously

Fraud tactics change constantly, so the model can’t be a one-time build. Track detection rate, false-positive rate, and model drift on an ongoing basis, and retrain on a regular schedule using newly confirmed fraud and false-positive cases.

AI Fraud Detection Use Cases Across Industries

AI fraud detection is widely used across industries to identify suspicious activities, reduce financial losses, and improve security. Here are some of the most common applications:

1. Financial Services

AI monitors transactions, account activity, and customer behavior to detect credit card fraud, account takeovers, and money laundering attempts. It can identify unusual spending patterns, suspicious transfers, and high-risk activities in real time. This helps financial institutions reduce fraud losses and improve regulatory compliance.

2. E-commerce and Retail

AI analyzes purchase behavior, payment methods, and device information to identify fraudulent orders and fake accounts. It can detect stolen credit card usage, bot attacks, and return fraud before they impact revenue. This helps online businesses reduce chargebacks and improve customer trust.

3. Healthcare

AI reviews medical claims, billing records, and patient information to identify fraudulent activities and anomalies. It can detect duplicate claims, inflated treatment costs, and medical identity theft. This helps healthcare providers and insurers minimize fraud-related expenses and improve operational efficiency.

4. Government and Public Sector

AI examines tax filings, public records, and benefit applications to detect fraudulent claims and inconsistencies. It helps identify tax evasion, duplicate applications, and misuse of government programs. This improves transparency and ensures resources are distributed appropriately.

5. Gaming and Virtual Economies

AI tracks player behavior, account activity, and digital transactions to identify unfair or fraudulent activities. It can detect cheating, account sharing, and unauthorized trading of virtual assets. This helps gaming platforms maintain fair competition and secure digital ecosystems.

AI Fraud Detection Compliance and Regulatory Requirements

AI fraud detection systems handle some of the most sensitive data a business holds: payment details, identity documents, biometric data, and behavioral patterns.

Several regulations directly govern how this data can be collected, used, and acted on. Failing to meet these requirements can lead to legal issues, financial penalties, and project delays.

1. PCI DSS v4.0.1 (Payment Card Industry Data Security Standard)

Businesses that store, process, or transmit payment card information must comply with PCI DSS v4.0.1, which became mandatory in March 2025. For AI fraud detection, this includes maintaining detailed logs of AI-driven decisions and restricting access to cardholder data to authorized users and systems only.

2. GDPR Article 22 (European Union)

GDPR Article 22 gives individuals the right not to be subject to a decision based solely on automated processing if that decision has a legal or significant effect on them — such as blocking a transaction or freezing an account. In practice, this means AI fraud systems serving EU customers need a path for human review and a clear explanation of why a decision was made.

3. EU AI Act

The EU AI Act classifies many fraud detection and credit-risk systems as “high-risk” AI. High-risk systems carry obligations around transparency, human oversight, and documentation of how the model was built, tested, and monitored.

4. India: RBI Guidelines and the DPDP Act

DPDPA Compliance for Indian banks and NBFCs follows RBI’s fraud risk management guidelines, which expect a structured fraud monitoring system with defined escalation processes. Separately, the Digital Personal Data Protection Act, 2023 governs how behavioral, biometric, and device data used in fraud models can be collected, stored, and processed, with specific consent and data minimization requirements.

Depending on your industry and region, additional regulations such as PSD2, the Bank Secrecy Act (BSA), FinCEN reporting requirements, and SR 11-7 Model Risk Management guidelines may also apply to AI fraud detection systems.

A Practical Compliance Checklist

- Log every AI-driven decision with a timestamp and the reason for the flag

- Offer a human review path for any fully automated block or account freeze

- Limit who and what can query payment, identity, or biometric data

- Document model training, validation, and retraining history

- Define a data retention and deletion policy for biometric and behavioral data

- Add an explainability layer (such as SHAP) for any deep learning model used in decisions that affect customers

Compliance requirements vary by industry and geography and change over time, so businesses should confirm current obligations with legal counsel before deployment. This section explains general principles and is not legal advice.

Best Practices for Deploying AI Fraud Detection

Deploying AI in fraud detection at a large scale requires careful planning, strong infrastructure, and continuous monitoring. If companies follow the right best practices, they can reduce fraud losses, improve customer trust, and maintain smooth operations.

Below are the most important best practices for scaling AI-powered fraud detection successfully.

1. Define and Monitor Key Metrics

Before deploying AI fraud detection, businesses must clearly define what success looks like. Important metrics include fraud detection rate, false positive rate, and manual review rate. These numbers help measure how well the system is performing.

Regular monitoring ensures that the AI system balances security with customer experience. If false positives increase, genuine customers may get blocked. Continuous tracking allows quick adjustments to improve artificial intelligence for fraud detection.

2. Build a Strong Data Foundation

Data is the backbone of AI fraud detection software. Without high-quality and real-time data, even the best AI model cannot perform well. Businesses should invest in secure data storage, fast data pipelines, and proper data cleaning systems.

A strong data infrastructure ensures better performance of AI for financial fraud detection. It also supports smooth AI integration in fraud detection systems across departments.

3. Use a Hybrid Approach

Companies should not completely remove traditional rule-based systems. Instead, they should combine them with AI models. Rules are effective for handling known and simple fraud cases.

At the same time, AI detects complex and new fraud patterns that rules may miss. This hybrid strategy makes AI in fraud prevention stronger and more reliable.

4. Keep Humans in the Loop

AI should support fraud experts, not replace them. Human analysts are still important for reviewing complex or high-risk cases. Their feedback helps retrain and improve the AI system.

By keeping humans involved, businesses increase trust in AI fraud detection and improve long-term accuracy.

5. Prioritize Real-Time Speed

Fraud happens in seconds, so detection must also happen in seconds. Businesses must design systems for low latency and fast decision-making.

The faster the AI fraud detection software responds, the more fraud it can prevent. Real-time fraud detection using AI helps stop losses before they occur.

Future Trends of AI in Fraud Detection

The future of AI-powered fraud detection is becoming more intelligent, automated, and privacy-focused. As fraudsters use more advanced techniques, organizations are adopting smarter AI systems.

Below are the key trends shaping the future of AI in fraud prevention.

1. Explainable AI (XAI)

Explainable AI helps businesses understand why a transaction was flagged or blocked. This improves transparency, supports regulatory compliance, and builds trust among customers and stakeholders.

2. Behavioral Biometrics

AI will increasingly analyze typing speed, mouse movements, scrolling behavior, and touchscreen interactions. These unique patterns help verify user identity and detect unauthorized access more accurately.

3. Graph Analytics

Graph analytics enables AI to map relationships between accounts, devices, IP addresses, and transactions. This helps uncover hidden fraud networks, mule accounts, and coordinated fraud activities.

4. Continuous Authentication

Instead of verifying users only at login, AI will continuously monitor behavior throughout the session. Any unusual activity can be detected instantly, reducing the risk of account takeover and session hijacking.

5. AI-Based Decision Automation

Future AI systems will automatically respond to suspicious activities by blocking transactions, freezing accounts, or triggering alerts. This speeds up fraud prevention and reduces reliance on manual reviews.

By learning from shared insights, AI models become more robust and capable of preventing emerging threats across financial services, e-commerce, telecom, and other sectors.

Developer Bazaar Technologies’ AI Development Services for Fraud Detection

At Developer Bazaar Technologies, we help businesses build secure, scalable, and intelligent AI fraud detection solutions. From planning and development to deployment and ongoing optimization, we support every stage of your fraud prevention journey.

- Custom AI Fraud Detection Software: We develop tailored AI fraud detection systems based on your industry requirements, transaction patterns, and risk profile to improve detection accuracy.

- End-to-End AI Integration: Our team seamlessly integrates AI into banking, fintech, e-commerce, insurance, and other digital platforms without disrupting existing operations.

- AI-Assisted Development: By leveraging AI-assisted development, we accelerate project delivery while maintaining high performance, reliability, and quality standards.

- Cost-Optimized AI Solutions: We build scalable and budget-friendly AI solutions that help businesses maximize ROI while keeping costs under control.

- Ongoing Monitoring and Support: Our team provides continuous monitoring, model optimization, and support to help your fraud detection system adapt to evolving threats.

Partner with Developer Bazaar Technologies to build future-ready AI fraud detection systems that protect your business and customers.

Conclusion

As digital transactions, online services and cloud platforms continue to grow, fraudsters are becoming more sophisticated and harder to detect using traditional rule-based systems. Artificial intelligence in fraud detection provides the speed, intelligence and adaptability required to identify suspicious behavior.

From financial services and e-commerce to healthcare and government sectors, AI-powered fraud detection is helping organizations strengthen security and meet regulatory requirements. With advanced features, AI offers a smarter and more scalable approach to fraud prevention.

However, successful deployment requires careful planning, strong data infrastructure, regulatory compliance and continuous monitoring. By following best practices and partnering with an experienced AI development company, businesses can build secure and future-ready fraud prevention systems.

FAQs

1. Can small and medium businesses use AI for fraud detection?

Yes, AI fraud detection is accessible to SMBs through scalable and cloud-based solutions. These systems can be tailored to match their transaction volume and risk level.

2. Does AI eliminate fraud?

No system can fully eliminate fraud. However, AI significantly reduces risks by detecting suspicious activity early and responding in real time.

3. What type of data is required for AI fraud detection?

AI systems use transaction data, user behavior patterns, device details, and historical fraud records. High-quality and structured data improves model accuracy.

4. Which AI algorithm works best for fraud detection?

There’s no single best algorithm. XGBoost and Random Forest are the standard choice for scoring individual transactions, while Graph Neural Networks are better suited to detecting fraud rings and synthetic identities that span multiple accounts. Most production systems combine both approaches.

5. Is AI fraud detection compliant with GDPR?

It can be, but only if the system includes a human review option for fully automated decisions and can explain why a transaction was flagged, as required under GDPR Article 22.

6. Does AI fraud detection require PCI DSS compliance?

Yes, if the system processes, stores, or transmits payment card data. PCI DSS v4.0.1 requires logging of AI-driven decisions and strict access controls around cardholder data.

7. What factors affect the cost of building an AI fraud detection system?

Cost depends mainly on data volume and quality, the complexity of the chosen models (a single XGBoost model costs far less to build and maintain than a graph-based system), real-time infrastructure requirements, and the level of regulatory documentation needed for the industry.